Should I Stay or Should I Go?

For several weeks we've characterized equities as "fragile." Valuations are high, earnings are not convincing, the Fed is in a tight spot and now cracks in the economy are appearing. Let's dig in...

1. What’s Happening in Small Cap Land?

Source: TradingView. Through year-to-date 2024.

Frequent readers know that we continually follow the path of the Russell 2000 US Small Caps due to their economic sensitivity.

In other words, US equity investors often express their economic growth views through their allocations to Small Caps.

With that in mind, it should be noted that Small Caps:

a) peaked over a month ago (March 28);

b) have seemingly reacted to the change in US Fed rate cut expectations (fewer cuts / higher for longer) more than their large-cap cousins;

c) failed as they tried to move above their early 2022 highs;

d) are potentially forming a “head and shoulders” top formation (similar to the Nasdaq 100 Equal Weight Index that we showed on Monday).

We see a meaningful move below $192 and back into the main 2022 / 2023 trading range as not only a negative for the Small Caps but potentially as a warning sign about the health of the US economy overall.

With that in mind, I recently had a discussion with the Portfolio Manager of one of the largest US Small Cap funds.

The conversation started with Fed policy - will the Fed cut rates this year?

My argument was that inflation (too high); unemployment (too low); and US equity markets near their all-time highs, in isolation, often warrant a hike (see here).

The Portfolio Manager referenced accelerating credit card delinquencies and sub-prime auto defaults as possible reasons for a cut.

In other words, his arguments for a cut (or at least not a hike) were that economic storm clouds were on the horizon.

A couple of weeks ago, we wrote that two words that we had not heard lately from investors were valuation and recession. (here).

This conversation put recession back on my radar at a time when many have taken a soft or no-landing for granted.

(This is not a recommendation to buy or sell any security and is not investment advice).

2. AI: What’s Priced In…

Source: Evercore. Through year-to-date 2024.

On Monday, we wrote about Magnificent 7 earnings vs. the earnings of the other 493 companies (of the S&P 500). (here)

In that piece, we noted that consensus estimates call for the Magnificent 7’s earnings to grow 37% in 2024 versus 1% for the other 493 companies and we commented that the challenge, in our view, is that a significant portion of this is likely priced in.

The chart above shows the estimates for Hyperscale Capex spend.

This is essentially what the largest US companies focused on AI are planning to spend to build the infrastructure to train the models that are the foundation of AI.

When analysts see what the hyperscalers are planning to spend - not just next quarter (as shown above), but also for next year - they revise their estimates for Nvidia and others.

The point, as we wrote above and alluded to on Monday, is that the surprise factor is decreasing and harder to achieve.

Once again, this is to say, that yes, Magnificent 7 earnings are continuing to grow, but investors, ourselves included, are already pricing in 2025 expectations.

All of that said, one comment that I recently read and consider particularly interesting is from Dan Loeb, the founder of Third Point hedge fund:

“Unlike in past periods of technological paradigm shifts, this new technology favors incumbents who are deploying their financial and intellectual war chests to win the AI arms race.”

In other words, start ups and smaller companies do not currently have the financial strength to compete with the Magnificent 7 in AI investment. (See the capex spend on the chart above).

While 2025 may be priced in, we continue to have selective exposure to the Magnificent 7 for longer-term AI upside.

(This is not a recommendation to buy or sell any security and is not investment advice. Please do your own due diligence).

3. We Found Our Answer, And We Weren’t Far Off: Oil

Source: Bloomberg. Through year-to-date 2024.

I did not plan to show the chart of oil today, but the break below $81 per barrel warrants attention and, for the most part is good news.

When considering oil price, we always highlight the correlation with inflation and inflation expectations.

So, too, does the Biden administration.

Two weeks ago (here), we highlighted oil when it had (in our view, somewhat unexpectedly) come down from $85 to $81 despite heightened tensions (bombs flying from Iran to Israel) in the Middle East.

We posited three possible reasons for the unexpected move lower:

“Was the move lower because economic growth prospects have been reduced given a tighter than expected Fed?

Was it because the bombs from Iran were largely intercepted and, therefore there is a lower likelihood of escalation?

Was it because the Biden administration knows the sensitivity of the US electorate to oil prices and has been aligning itself more with Saudi Arabia (notice the coordination in between the US and Saudi Arabia in defending Israel) to keep oil in check?”

Today, the Bloomberg headline is “US and Saudis Near Defense Pact Aimed at Reshaping Middle East.”

Clearly a big agreement with a broad scope.

While the proximate causes for the increased level of partnership were to help end the Israel / Gaza conflict and to provide Saudi Arabia with advanced arms (good for US military contractors), clearly increased oil supply is a part of the conversation.

In general, this is a positive that should help reduce inflation, which can take pressure off of the Fed and potentially ease 10-Year yields. It is also a win for the Biden administration.

It’s also possible, given the theme of today’s note, that reason number 1 I provided for the drop in oil price - economic slowdown - is partially responsible. We will see.

(This is not investment advice or a recommendation to buy or sell any security).

4. Starbucks

Source: TradingView. Through year-to-date 2024.

After reporting earnings last night, Starbucks shares dropped 17% today and are down 36% from their May 2023 high.

If there’s a silver lining, it’s that shares are back near a level that has acted as a floor in the past.

We don’t often show charts of individual stocks and the point of this one is to consider whether we should extrapolate Starbucks performance to the health of the consumer and to the economy overall or, if Starbucks performance was simply due to poor execution and competition.

First, the earnings highlights: company wide same store sales fell 4% and traffic fell 6% for the quarter; China same store sales plunged 11% with an 8% decline in the average order; and management lowered revenue growth guidance from 7% to low-single digits for the year.

The management team made this comment: "Most loyal customers are looking for discounts" and most people that I have read have reacted to the earnings report by saying the price at the stores is too high.

While it is clear that China and the overall international business is challenged, we don’t want to ignore the fact that Starbucks will have difficulty passing along any potential future price increases.

Although it is early to extrapolate this to the broad economy, it is increasingly clear both from the comments of my Small Cap Manager friend (chart 1), oil and Starbucks that we need to keep our eye on the consumer and the economy overall.

(This is not a recommendation to buy or sell any security, please do your own research).

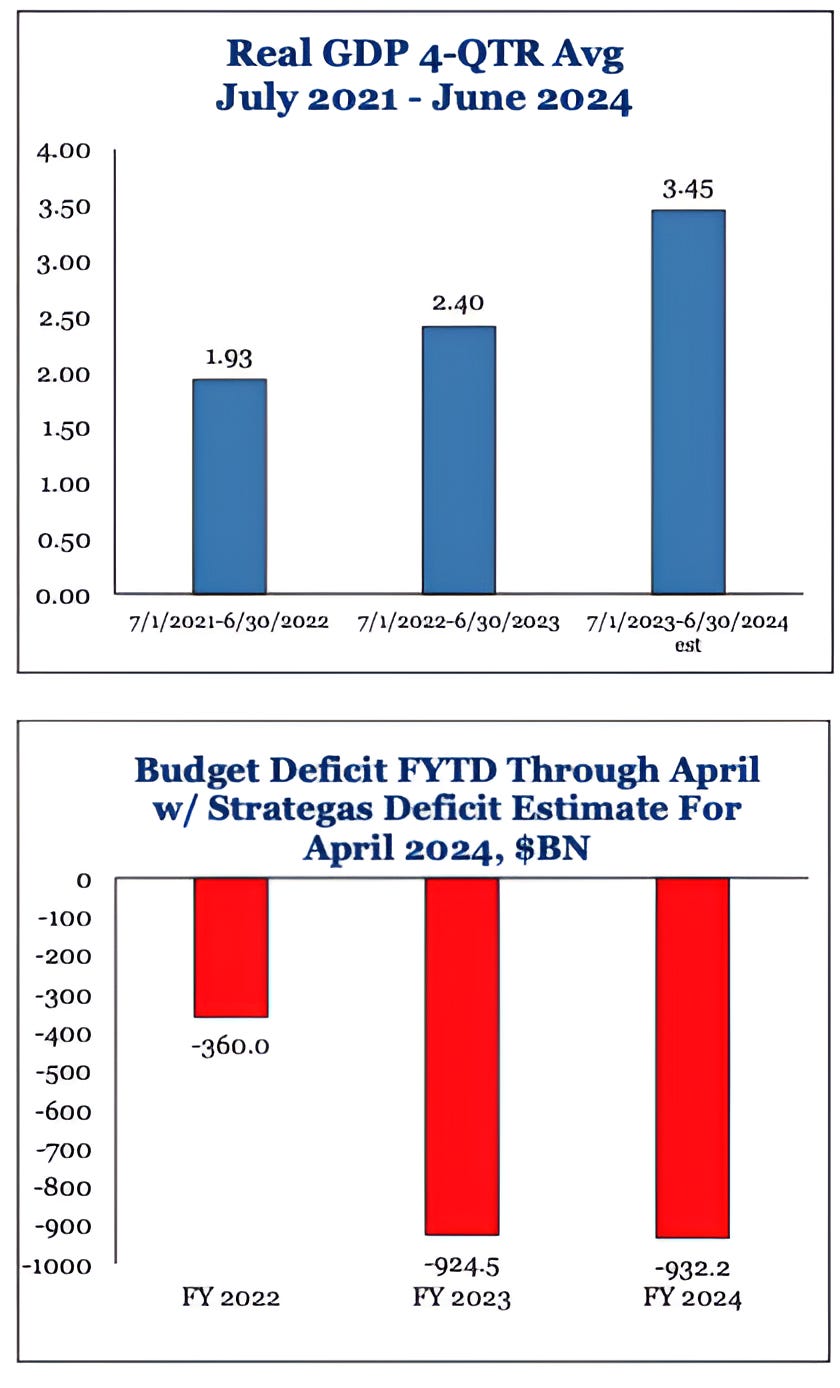

5. Growth Isn’t Helping the Deficit

Source: Strategas. Through year-to-date 2024.

The charts above from Strategas show US growth (top) and budget deficits (bottom).

In general, with US economic growth accelerating from 2.4% to 3.5% in the past 12 months, the deficit should be declining.

Tax revenues are growing, but spending is growing more, and, as a result, economic growth is not bringing down the deficit.

We continue to emphasize this not just because one of our themes is Fiscal Dominance (here) but because this could impact Fed policy decisions (here) and, may at some point result in higher 10-Year yields.

Higher 10-Year yields are often consistent with lower equity valuations and multiples. (Past performance is not indicative of future results).

In an equity market environment that we have characterized as fragile, the US budget deficit and interest payments are (or will become) a key consideration for investors (both equity and fixed income).

(This is not a investment advice and is not recommendation to buy or sell any security).