Slow Down, Take It Easy...

Has the post-election rally gone too far, too fast? The sectors that outperformed in November 2016 are outperforming again, but valuation and the charts are very different this time. Let's dig in...

Over the past week, the S&P 500 is up over 4% (the best week of the year) and several indexes our approaching our near-term targets.

Given the velocity of the move north, we would not be surprised to see a pause at the very least and, possibly some profit taking.

While we don’t expect a significant near-term drawdown, we are once again adding puts and put spreads to our portfolios.

From time to time, these puts and put spreads are a drag on performance, but they allow us to remain invested and sleep at night. Furthermore, when they pay off, they cover the profit drag and then some.

For those that have not fully participated in the rally, we do not see this as an optimal time to add.

With that said, I want to reiterate what I wrote last Thursday (I have adjusted the numbers to reflect today’s data, but the point remains):

When Trump won the election in 2016, the S&P 500 was trading at 16.5x next 12 months earnings. Today, it is at 22.8x (see chart 4).

Comparing today’s 10-Year Treasury yield of 4.39% with that in 2016 of 2.25% (right after Trump won the election), there is also a notable difference.

This means that the equity risk premium - the amount that investors are being paid to take equity risk rather than invest in “risk free Treasuries” - is much lower today than it was when Trump won in 2016.

In other words, both the absolute and relative (to Treasuries) valuations of US equities today are much more expensive now than they were in November 2016. While this is not insurmountable, it is a significant headwind.

Slow down, take it easy!

1. The Equal Weight S&P 500: Approaching Our Target

Source: Trading View. Through year-to-date 2024.

The chart above shows the Equal Weight S&P 500 (ticker: RSP).

We always monitor the Equal Weight S&P 500 to see how the “average” S&P 500 stock is doing. We last showed this here.

The Equal Weight S&P 500 ETF traded in a broad range from its January 2022 peak to March 2024.

After moving above the range earlier this year, the Equal Weight S&P 500 came back down and “retested” its former ceiling level. (We often write about retests and wanted to highlight one).

With the 50 basis point Fed rate cut in mid-September, the average stock finally found true escape velocity.

The Equal Weight S&P 500 ETF is now approaching the 1.618 Fibonacci extension of its 2022 sell-off at $188 which we consider to be the first target for the ETF.

Although we expect a pause and consolidation around that level, our slightly more distant target for the Equal Weight S&P 500 ETF is $192. This is based on simple symmetry from the $162 January 2022 high to the $132 October 2022 low. ($162 + ($162-$132))

While the average stock continues to do well, in our view, near-term gains may be somewhat constrained.

(This is not a recommendation to buy or sell any security and is not investment advice. Past performance is not indicative of future results. Please do your own research and due diligence).

2. Financials: First Target Hit!

Source: Trading View. Through year-to-date 2024.

The chart above shows the Financial Sector ETF (ticker: XLF).

We last showed the Financial ETF relative to the S&P prior to the election (here). At the time, we said:

“In our view, a portion the rally since August and a justification for the recent outperformance may be due to investors considering a Trump victory.

Financials were one of the best performing sectors after Trump won the 2016 US Presidential election.

With Financials hovering at the Maginot line, investors may be waiting for the election outcome to determine the next move in Financials relative to the S&P 500.”

Since the election, the Financial Sector has rallied both absolutely (chart above) and relatively.

Unlike the The Equal Weight S&P 500 ETF, the Financial Sector ETF has achieved our initial target.

Similar to the The Equal Weight S&P 500 ETF (and the major indexes), our initial target for the Financial Sector ETF is the 1.618 Fibonacci extension level of its 2022 sell-off. In our view, the ETF is likely to pause at this level.

However, after a battle, that we expect to be shorter than the four month battle at the January 2022 high, we would not be surprised to see the Financial Sector ETF move towards $52.50.

$52.50 is a target established considering symmetry of the 3-year sideways move between the pre-covid peak of $30.50 and the January 2022 high of $41.50. ($41.50 + ($41.50-$30.50)).

(For lynx eyed chart observers, you will note a similar symmetry after the April 2022 to December 2023 range).

So our view with respect to Financials is: a) pause; b) may sell-off a little; c) move sideways; d) re-attack the $49.50 area; and e) eventually hit $52.50.

Finally, for those interested, the top 5 positions in the Financial Sector ETF are: Berkshire Hathaway (12.8%); JP Morgan (9.8%); Visa (7.5%); Mastercard (6.4%); and, Bank of America (4.4%).

(Past performance is not indicative of further results. This is not a recommendation to buy or sell any security and is not investment advice. Please do your own due diligence).

3. Does Expected Revenue Growth Justify Expected Earnings Growth?

Source: Strategas. Through year to date 2024.

The chart above shows the quarterly S&P 500 revenue growth: actuals from Q1 2023 to Q2 2024; preliminary for Q3 2024; and estimates for Q4 2024 through Q3 2025.

While they are from two different data sources, Q3 revenues (from IBES) are estimated to grow 5.3% while earnings (from FactSet) are growing 4.2%. (I have seen some say that Q3 earnings growth is higher than 4.2% - I track this number weekly from FactSet and this is what the FactSet data shows)

(As an aside, the IBES future quarterly earnings growth estimates are similar to the FactSet future earnings growth estimates).

I most recently showed quarterly earnings estimates here and quarterly earnings growth estimates here (this is from two months ago, although the trajectory hasn’t changed, the magnitude has come down slightly).

The point here is that S&P 500 revenues growth expectations seem stable (and even slightly declining) at around 5% while earnings growth is expected to move from an average of 6% over the last four quarters to an average of 13% over the next four quarters.

The earnings growth can come from: a) cost cutting that leads to margin expansion; b) share buybacks that lead earnings per share higher; or c) from a corporate tax cut (Bank of America sees current Trump proposals as 4% accretive).

We don’t currently see any of these three factors adding meaningfully to 2025 earnings growth.

We have highlighted our concern with the 2025 earnings growth expectations for some time (see here; here; chart 3 here; chart 3 here; charts 2, 3 and 4 here; chart 3 here; and chart 3 here) and we view the revenue growth projections shown above as one of the factors that leads us to that view.

(Past performance is not indicative of future results. This is not a recommendation to buy or sell any security and is not investment advice. Please do your own due diligence).

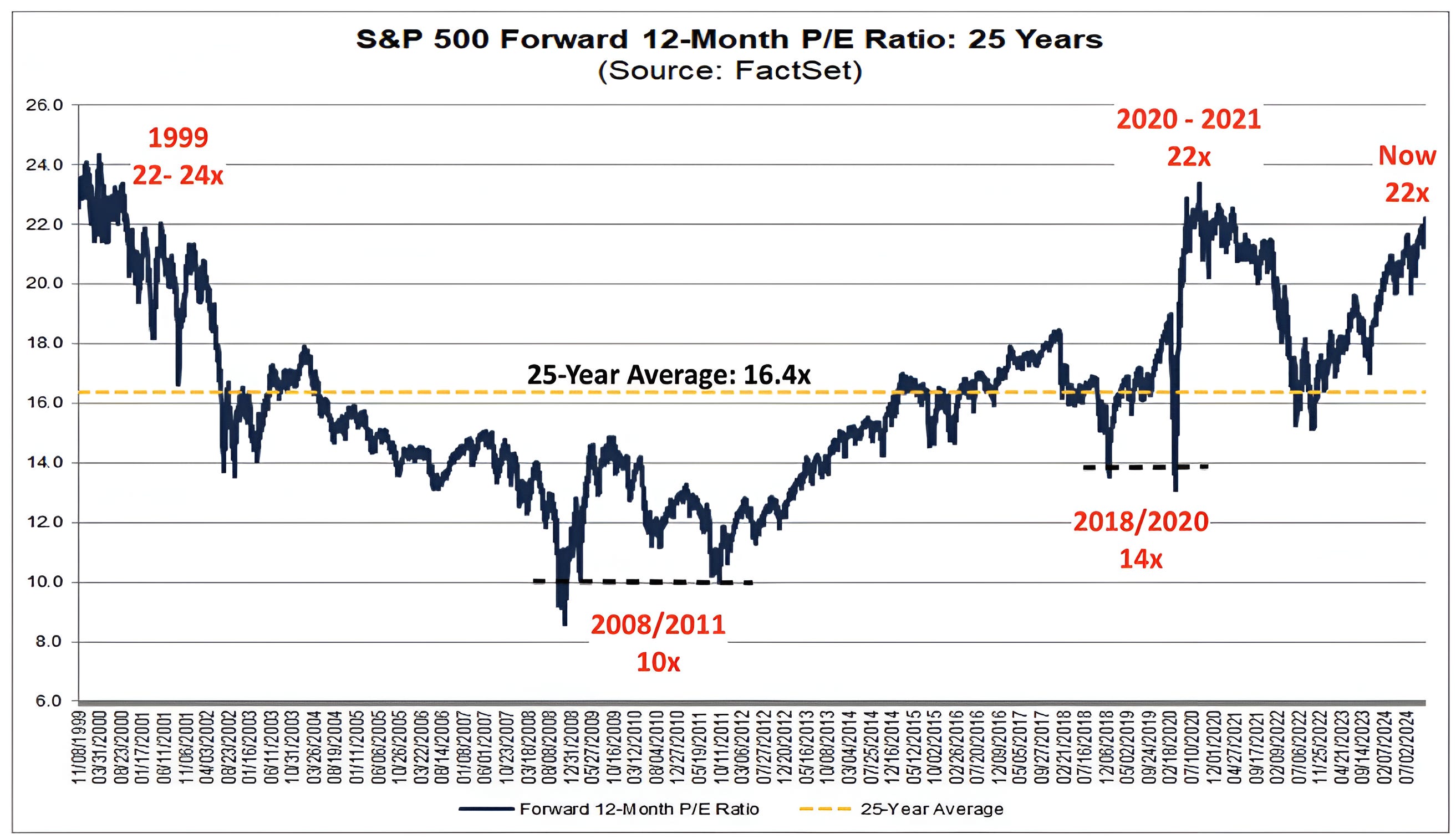

4. Valuation is Officially Elevated!

Source: FactSet. Through year-to-date 2024.

The chart above shows the S&P 500 Price to next 12 months Earnings (“Price to forward earnings” or “PE”) over the past 25 years.

We have highlighted valuation several times in the past including chart 3 here; chart 4 here and chart 4 here.

In our view, over the past 25 years, there have been three valuation bubbles in the S&P 500: 1) the dot.com bubble 1999 / 2000; 2) the post-covid bubble 2021; and 3) today (simply observing the chart above).

While valuation in the prior two bubbles was able to remain elevated for an extended period (~1 year+), each time, the imbalance was resolved as valuation moved lower.

When highlighting valuation, typically, the first thing we write is that valuation is not a catalyst. An expensive market will not go down because its expensive and a cheap market will not go up because it’s cheap.

There is usually a trigger.

In 2000, companies began to miss earnings expectations and in 2022, the Fed tightened.

Will this time is different? Can valuation remain higher for longer? Can the PE multiple expand further? Will the pin that pricks the bubble look different than those in the past?

While we do not know, in our view, it is likely that there will be a resolution at some point that leads the valuation of the S&P 500 to revert lower.

As a further qualification to valuation not being a catalyst, we would also say it is not a timing tool.

In other words, simply because valuation is elevated, does not mean that we need to sell today. It does mean we need to be aware.

To help with timing, we watch the charts and inter-market relationships.

(Past performance is not indicative of future results. This is not a recommendation to buy or sell any security and is not investment advice. Please do your own due diligence).

5. A Long Look at the Brazilian Real

Source: Trading View. Through year-to-date 2024.

The chart above shows the Brazilian Real (BRL) / US dollar cross from 2000.

I began working for Itau in 2008 when the BRL was around 1.80 to the US dollar.

My Brazilian colleagues would visit New York and return home with new suitcases full of Nike, Apple and Abercrombie goods.

At the time, there was a magazine article that highlighted a strategy for couples that were expecting a baby to save money by visiting the US for a weekend and buying everything for the newborn there. The savings outweighed the cost of the flight and the hotel (depending on the length of the stay).

When the Real weakened to 2.10, I encouraged people to buy dollars. They wanted it to go back to 1.90 or 2.00. At 3.00, they wanted to wait for 2.50.

After covid, as can be seen in the chart, the BRL moved through 4.00 and established a new range from 4.90 to 5.80. It is now flirting with the top of that range.

Although I have spent considerable time in Brazil (and I love the country), it would be naive of me to say that I understand all of the factors that feed into the exchange rate.

That said, simply looking at the chart above and applying the same simple symmetry that we applied to the Equal Weight S&P 500 and the Financials (charts 1 and 2 above), we would say that if the BRL were to move above its 4.5 year sideways range, our target would be 6.70 (5.80 + (5.80-4.90)).

Importantly, the BRL has NOT moved above that range.

Furthermore, this is not a prediction, it is an observation based on the chart. It is presented simply as something to consider.

(Past performance is not indicative of future results. This is not a recommendation to buy or sell any security, please do your own research).